Report on the alternative dispute resolution activity as at 30.09.2019

The first three quarters of 2019 observe a constant development of the work of the Alternative Banking Dispute Resolution Centre (ABDRC). The applications received before the end of Q3 2019 point to a 130% increase compared to the number of applications received during the entire previous year. As regards the casefile formed, during the three quarters, these already accounted for 95% of the total number of casefiles formed in 2018. A special category is represented by the amicable settlements occurred between consumers and banks, having first referred the matter to ABDRC. To date, the parties entered into more than 183 such settlements, compared to only 97 settlements during the entire previous year (2018).

* for year 2019, the figures are those reported in the end of Q3. For years 2016, 2017 and 2018, the figures are those reported in the end of the respective year.

* for year 2019, the figures are those reported in the end of Q3. For years 2016, 2017 and 2018, the figures are those reported in the end of the respective year.

* for year 2019, the figures are those reported in the end of Q3. For years 2016, 2017 and 2018, the figures are those reported in the end of the respective year.

* for year 2019, the figures are those reported in the end of Q3. For years 2016, 2017 and 2018, the figures are those reported in the end of the respective year.

In the end of Q3 2019, as many as 328 consumers made peace with their banks or NBFIs with the help of ABDRC, meaning 130% more consumers than in the end of Q3 2018. During the same period of last year, only 252 Romanians benefited of favourable solutions following the negotiations carried out with the financial and banking institutions.

Since the beginning of the year, 1,676 Romanian submitted to ABDRC applications for amicable settlement of their disagreements with banks or NBFIs, which points to an increase of 195% compared to the similar period of last year. In the first three quarters of 2018, only 862 compliant applications were received. Overall, more than 5,200 people asked information from (including by phone) and approached the Centre in the first three quarters of 2019. Compared to the similar period of 2018, the number of casefiles formed went up by 130%.

The online possibilities to submit applications (the application available on the website www.csalb.ro, as well by email [email protected]) were the option of choice for 85% of the Romanians who submitted applications to ABDRC.

Of the total number of compliant applications received in Q1-Q3 2019, 1,392 concerned issues related to their relation with the bank, whereas 284 concerned different issues occurred between consumers and NBFIs.

The total number of casefiles formed in Q1-Q3 2019 reached 522, of which 514 involved banks, and only 8 such casefiles concerned NBFIs, during the indicated period. Compared to the similar period of 2018, the number of casefiles formed went up by 30%.

- Of the casefiles involving banks thus formed, 325 concluded with a resolution (the parties accepted the solution proposed by the conciliator), while other 130 casefiles are currently in processing/resolution stages. In 40 casefiles, the parties rejected the solution the conciliator rendered, and a procedure closure report was consequently issued, whereas in 16 cases one of the parties withdrew from the procedure.

- Of the 8 casefiles involving NBFIs formed, 3 concluded with a resolution, and a procedure closure report was issued in only one case; 4 other casefiles are still being discussed with the parties.

Furthermore, 183 applications were settled amicably by traders, but after having first approached ABDRC (traders negotiated directly with consumers), broken down as follows: 159 applications settled amicably with banks, and 24 applications settled amicably with NBFIs.

In the end of Q3 this year we counted approximately 3,600 queries by phone.

Their break-down on banks/NBFIs is as follows:

Banks:

- 1,392 compliant applications;

- 47 non-compliant applications;

- 680 queries for various information.

NBFIs:

- 284 compliant applications;

- 10 non-compliant applications.

Qualification of the 1,392 compliant applications concerning banks:

- 514 applications turned into casefiles;

- 159 applications settled amicably by the trader after the consumer referred the case to ABDRC;

- 66 in screening phase – documents are being reviewed (the rest are closed applications).

Qualification of the 514 casefiles undergoing the procedure with proposed solution (involving banks):

- 325 resolutions rendered – the parties reached an agreement (approximately 90% of the total solutions);

- 131 casefiles in the phase of processing/discussions with the parties;

- 40 reports issued – the parties did not reach an agreement (approximately 10% of the solutions rendered);

- 16 casefiles in which one party withdrew from the procedure.

Qualification of the 284 compliant applications concerning NBFIs:

- 103 in screening phase – documents are being reviewed;

- 24 applications settled amicably by the trader after the consumer referred the case to ABDRC;

- 8 applications turned into casefiles (the rest are closed applications).

Qualification of the 8 casefiles undergoing the procedure with proposed solution (involving a NBFI):

- 4 casefiles in the phase of processing/discussions with the parties;

- 3 resolutions rendered – the parties reached an agreement;

- 1 report – the parties failed to reach an agreement.

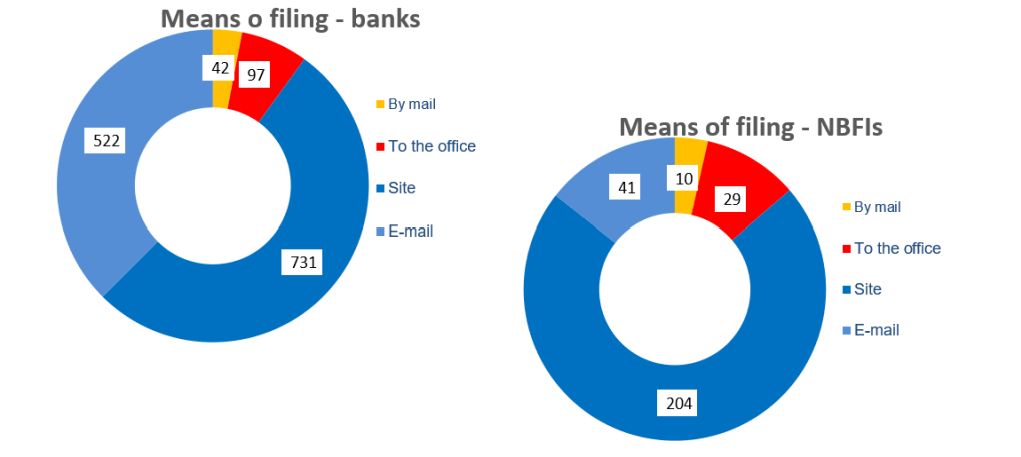

Means of filing compliant applications (involving both banks and NBFIs):

- 935 were submitted via the app (website);

- 563 were emailed;

- 126 were brought to, and registered by consumers with the office of ABDRC;

- 52 were mailed.

Most of the applications received from customers concerned:

- Issues with the loans taken – 90%

- Reduction of loan principal

- Removal of fees (management, monitoring fees)

- Repayment of fees (management, analysis, risk, monitoring fees)

- Interest recalculation

- Termination of contractual provisions

- Issues concerning foreclosure

- Rescheduling, repayment or re-staging-out of loans

- Reinstatement of repayment schedule

- Repayment of amounts

- Deregistration from the Credit Register

- Other issues – 10%

- Deposits

- Credit cards

- Current account

- Problems with bank transfers

- Leasing

The main reasons for closing compliant applications are:

- Traders (both banks and NBFIs) refused the settlement of the dispute via ADR procedures because:

- he trader maintained their opinion submitted to the consumer before the referral to ABDRC (157 cases);

- several offers and settlement attempts have been made, but all the offers submitted before the referral of the matter by the consumer to ABDRC were turned down by the latter (59 cases);

- pending court proceedings (34 cases);

- foreclosure proceedings have already been initiated (23 cases).

NOTE:

The interest shown by consumers in ABDRC (as evidenced by the number of applications and referrals) almost doubled compared to the same period of last year. The figures for the end of Q3 this year, compared to those of the same period of last year, are 94% better in terms of the number of applications received. If we are to look into the cases resolved (by resolutions, or by amicable settlement after a referral to ABDRC), their number increased by 75%. As regards the number of casefiles formed, the end of Q3 2019 observes an increase by 30% v. end of Q3 2018. End of Q3 2019 reports a monthly average which is better than the average of the entire 2018, in respect of both the number of applications, as well as the number of casefiles formed .

|

Q3 2018 in figures:

(All) 2018 in figures:

|

Q3 2019 in figures:

|

STATISTICAL INFORMATION IN THE END OF Q3 2019:

CONCLUSIONS:

The work of ABDRC continues the ascending trend of 2018 with a strong increase in the number of applications received, casefiles formed, resolutions rendered, and amicable settlements reached between consumers and banks.

The key drivers of these developments are: more sources of information about the work of the Centre available to consumers and greater openness of banks to conciliation.

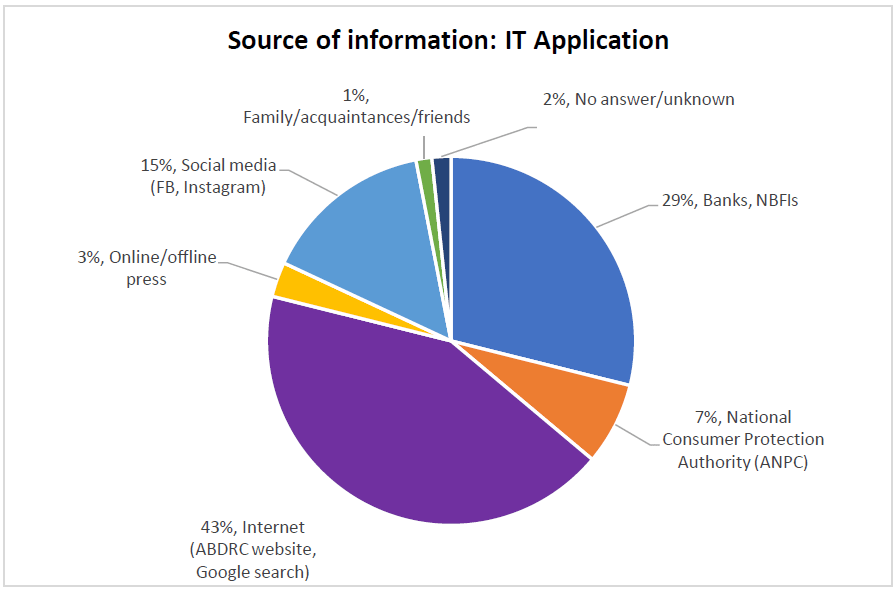

Part of the IT App (available on the website www.csalb.ro) which consumers can use to submit applications to have their disagreements with banks/NBFIs resolved, users are questioned about their sources of information about ABDRC. 58% of consumers found out about the existence and benefits of the Centres in the online environment, whereas 29% of them received such information from banks or NBFIs.

The ranking returned by the IT App, based on the answers of 360 users, is as follows:

- Internet (ABDRC website, Google search) – 43%

- Banks, NBFIs – 29%

- Social media (FB, Instagram) – 15%

- National Consumer Protection Authority (ANPC) – 7%

- Online/offline press – 3%

- No answer/unknown – 2%

- Family/acquaintances/friends – 1%

The WEBSITE www.csalb.ro has made available to consumers since July 2018 an online application which allows for faster and smoother submission of the conciliation applications. On the first page of the website, consumers are prompted to access this application by filling in an application. The documents entered in the registration form are uploaded into the online application, and then processed within approximately one hour. By email, the classic procedure, documents used to be processed in approximately one day. The online application was setup in observance of the principles of the General Data Protection Regulation (GDPR).

The Alternative Banking Dispute Resolution Centre (ABDRC) is an independent non-governmental, apolitical, and not-for-profit legal entity of public interest established under the Government Ordinance no. 38/2015 on alternative resolution of disputes between consumers and traders, which transposes at domestic level Directive 2013/11/EU on alternative dispute resolution for consumer disputes and amending Regulation (EC) no. 2006/2004 and Directive 2009/22/EC.