During the first three months of 2026, as many as 231 consumers went through the entire conciliation process: application filing, negotiation, final resolution ó a solution accepted by both parties in 150 cases, or reached an amicable settlement directly with their banks/NBFIs, having first approached ABDRC (in 81 cases).

In the first three months of the year, 29 court cases were terminated because the parties wanted and managed to find an amicable solution with the help of ABDRC.

The number of applications recorded in the first three months of the year (968 applications) shows a slight QoQ increase of approximately 6% in the current year, compared to Q1 2025 (916 applications). Some consumers continued to experience genuine difficulties in making the due payments, and these justified circumstances required identification of solutions to rebalance the contractual obligations (with the applications being submitted directly to creditors, or via ABDRC).

Of the total number of applications received by the end Q1 2026, 717 concerned different issues in relations with banks, whereas 251 concerned different issues in relations with NBFIs.

Thus, the share of applications intended at NBFIs slightly increase above last year’s reference period: from 21% of total/Q1 2025 up to approximately 26% of total/Q1 2026.

Moreover, the share of applications intended at banks observes a slight decrease in the two periods subject to comparison: 79% of total/at the end of Q1 2025, and 74% of total/Q1 2026.

In this statistical slot, we need to highlight also that, in the first three months of this year, the applications for deregistration from the Credit Bureau (CB) observed a slight 3M/3M upward trend.

At the end of Q1 2026, we see 177 applications for deregistration from the Credit Bureau (107 intended at banks + 70 intended at NBFIs), while the number of this type of applications recorded at the end of Q1 2025 was 155. It should be recalled that most of the applications aimed at deregistration from the Credit Bureau are closed because there is a special law in place for these cases, and this prevents such negotiations.

The number of casefiles formed at the end of Q1 2026 reached 197, all of which concern banks. By way of comparison, 189 casefiles were formed in the first three months of 2025, which means an increase by approximately 5% of this statistical indicator in the current year. Of the casefiles formed this year and settled until the end of the reference period, 150 concluded with a resolution (the parties accepted the solution proposed by the conciliator), while other 35 casefiles are still being processed (at the end of Q1 2026). In 8 cases, one of the parties rejected the solution the conciliator rendered and a report was issued, whereas in 4 cases, one of the parties withdrew.

The number of resolutions handed down in the first quarter of this year is 150, compared to the figure reported for the same period of last year, i.e., 143 resolutions (during the two periods under review, being Q1 2026 and Q1 2025, the share of resolutions out of the total solutions is 95%/Q1 2026 and, respectively 99%/Q1 2025).

Furthermore, before the end of Q1 2026, 81 applications were settled amicably by traders after the respective cases having been referred to ABDRC (traders negotiated directly with consumers), broken down as follows: 65 applications settled amicably with banks, and 16 applications settled amicably with NBFIs.

At the end of the Q1 of this year, we counted approximately 723 enquiries made by phone, and 162 persons/consumers accessed the chat function on the website of ABDRC.

A breakdown of the applications by traders looks as follows:

Banks:

- 717 compliant applications;

- 36 non-compliant applications;

- 593 requests for miscellaneous information.

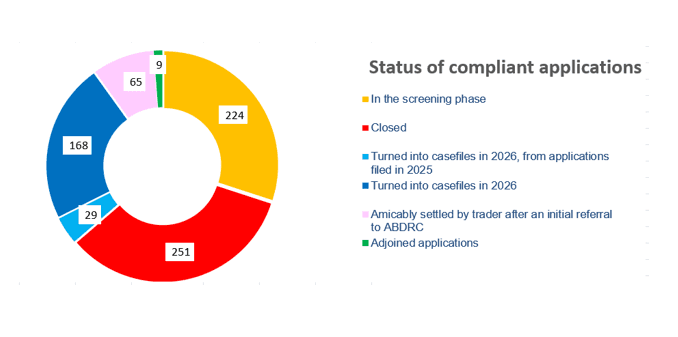

Classification of the 717 compliant applications:

- 197 cases formed in the end of Q1 2026 (at the start of 2026, 29 casefiles were formed from compliant applications received in late 2025);

- 224 applications in screening phase – documents are being reviewed;

- 65 applications were settled amicably by the parties, but this after the consumer having first approached ABDRC;

- 251 cases were closed;

- 9 applications were joined.

Classification of the 197 casefiles pending in the procedure with proposed solution/conciliation:

- 150 resolutions were handed down – the parties came to terms;

- 35 casefiles are in the processing phase;

- 8 reports – the parties failed to reach an agreement;

- 4 casefile in which one of the parties withdrew.

Methods of filing compliant applications – regardless of the referral channel, all compliant applications are entered into the IT application used to manage applications and casefiles:

- 446 were submitted via the app (website);

- 175 were emailed;

- 83 were mailed;

- 13 were brought to, and registered by consumers with, the head-office of ABDRC.

NBFIs:

- 251 compliant applications;

- 11 non-compliant applications.

Classification of the 251 compliant applications:

- 37 applications in the screening phase;

- 16 applications were settled amicably between NBFIs and consumers, after the consumer having first approached ABDRC;

- 198 were closed – rejected by the NBFIs.

Means of filing compliant applications:

- 224 were submitted via the app (website);

- 26 were emailed;

- 1 was brought to, and registered by the consumer at, the office of ABDRC.

The applications received from consumers covered the following topics:

- Problems in connection with credit products:

- Refunds (of fees/commissions, interest);

- Reduction of loan principal/debt/instalment, or writing off overdue amounts;

- Rescheduling/refinancing/staging-out;

- Agreement renegotiation/rebalancing (including for hardship);

- Finding a solution to address the problems (in general);

- Shift from ROBOR to IRCC;

- Conversion of the loan currency;

- Problems with insurance policies (bancassurance);

- Interest recalculation;

- Payment commitments;

- Maturity acceleration;

- Removal of certain clauses;

- Credit Bureau (deregistration from CB).

- Operational problems:

- Problems with operation of the ATMs (including refunds);

- Problems in connection with wire transfers and refunds of transaction fees;

- Refunds in case of processing errors;

- Recovery of amount wrongly transferred by consumers (internet banking);

- Provision of clarifications about calculation of the amounts withdrawn by banks from the credit card account;

- Other card-related problems (cancellation/name change);

- Problems in connection with the exchange rate and interests charged when using the cards abroad;

- Problems regarding inter-banking transfers.

- Problems related to other types of activities:

- Problems in connection with forced execution (suspensions/stays of proceedings);

- Requests to be issued documents (repayment schedules, statements of account, mortgage deregistration, etc.);

- Refunds of garnished amounts;

- Fraud committed via bank channels.

The main reason for closing an application is the refusal of traders to have the dispute settle via ADR procedure, and the reasons for closing fall into several categories:

- Good reasons (main) – the application concerns:

- deregistration of entries from the Credit Bureau;

- “First Home” loans;

- claim assigned to companies which are not regulated by the National Bank of Romania;

- the state premium under saving-credit contracts.

- Reasons related to consumers:

- selection of a trader the business of which is not regulated by the National Bank of Romania;

- selection of a trader they don’t have commercial relations with;

- the information/documents required for resolving the application have not been supplied;

- the consumer does not reply within 90 days, or withdraws during negotiations.

- Other reasons:

- pending court proceedings;

- forced execution procedures have already been initiated;

- while traders made several offers, all of them were turned down by consumers (before referring the matter to ABDRC), and traders maintain their point of view in the initial answer;

- lack of grounds (claimed by the trader).

BENCHMARKING:

| Q1 2025 in figures:

· 916 compliant applications – 305 applications per month; · 143 casefiles concluded with resolutions/the parties coming to terms (an average of 48 resolutions/month), of 189 casefiles formed at the end of Q1 2025 (an average of 63 casefiles/month); · 57 applications settled amicably by the parties after an initial referral to ABDRC – (an average of 19 applications settled amicably and directly between the parties/month). 2025 in figures (entire year): · 2,866 applications – 239 applications per month; · 911 cases – 76 cases per month; · 336 applications settled amicably – 28 amicably settled applications/month. |

Q1 2026 in figures:

· 968 compliant applications – 323 applications per month; · 150 cases concluded with resolutions/the parties coming to terms (an average of 50 resolutions/month), of 197 casefiles formed at the end of Q1 2026 (an average of 66 cases/month); · 81 applications settled amicably by the parties after an initial referral to ABDRC – (an average of 27 applications settled amicably and directly between the parties/month).

|