Increase by more than 80% in Reconciliations between Banks and Consumers via ABDRC

The negotiations between consumers and banks via the Alternative Banking Dispute Resolution Centre (ABDRC) have run even faster this year, and the number of cases concluded with reconciliation of the parties has increased by more than 80% compared to the first half of 2020. The negotiation outcome follows the same increasing trend. In mid-year, the benefits of negotiations have already exceeded EUR 800 thousand, the largest half-yearly amount since the Centre was established. In fact, 95% of the negotiations conducted this year concluded with consumers and banks accepting the solutions proposed by conciliators. We welcome the piece of good news that, as of June, face-to-face negotiations involving consumers, representatives of banks and conciliators in the premises of ABDRC have been resumed.

21 July, Bucharest. The negotiations between consumers and banks via the Alternative Banking Dispute Resolution Centre (ABDRC) have run even faster this year, and the number of cases concluded with reconciliation of the parties has increased by more than 80% compared to the first half of 2020. The negotiation outcome follows the same increasing trend. In mid-year, the benefits of negotiations have already exceeded EUR 800 thousand, the largest half-yearly amount since the Centre was established. In fact, 95% of the negotiations conducted this year concluded with consumers and banks accepting the solutions proposed by conciliators.

“This year we see more willingness of consumers and banks to negotiated and make compromises in order to maintain their contractual relations, avoid court proceedings, and capture the benefits that, eventually, are obtained by both parties. We welcome the piece of good news that, as of June, face-to-face negotiations involving consumers, representatives of banks and conciliators in the premises of ABDRC have been resumed (photo in attachment). Coming back to figures, we can see an important difference v 2020. While in the first six months of last year there were 116 negotiations concluded with reconciliation of the parties, the first half of this year saw 211 cases where the parties reconciled. In other words, 92% of the negotiation casefiles formed this year have already been resolved, compared to only 50% in the same period of last year, and this proves that the banks’ alternative dispute resolution mechanisms have been fined-tuned, and the parties are more willing to reach an agreement. As to applications, the situation is similar to last year, but here some recommendations need to be made to consumers. They need to know that a negotiation applications filed without minimum details about the status of the loan or the situation of the family or of the borrower has little chances of being accepted by the bank. On the contrary, a detailed application having enclosed also copies of documents supporting the reported situation can boost the negotiation quality and the willingness of the banks to come up with solutions to address the problems reported by consumers. Additionally, this would also help the conciliator leading the negotiations propose a better solution in the end of the conciliation“, says Alexandru Păunescu, Chairman of ABDRC’s Steering Board.

“This year we see more willingness of consumers and banks to negotiated and make compromises in order to maintain their contractual relations, avoid court proceedings, and capture the benefits that, eventually, are obtained by both parties. We welcome the piece of good news that, as of June, face-to-face negotiations involving consumers, representatives of banks and conciliators in the premises of ABDRC have been resumed (photo in attachment). Coming back to figures, we can see an important difference v 2020. While in the first six months of last year there were 116 negotiations concluded with reconciliation of the parties, the first half of this year saw 211 cases where the parties reconciled. In other words, 92% of the negotiation casefiles formed this year have already been resolved, compared to only 50% in the same period of last year, and this proves that the banks’ alternative dispute resolution mechanisms have been fined-tuned, and the parties are more willing to reach an agreement. As to applications, the situation is similar to last year, but here some recommendations need to be made to consumers. They need to know that a negotiation applications filed without minimum details about the status of the loan or the situation of the family or of the borrower has little chances of being accepted by the bank. On the contrary, a detailed application having enclosed also copies of documents supporting the reported situation can boost the negotiation quality and the willingness of the banks to come up with solutions to address the problems reported by consumers. Additionally, this would also help the conciliator leading the negotiations propose a better solution in the end of the conciliation“, says Alexandru Păunescu, Chairman of ABDRC’s Steering Board.

APPLICATION DRAWING-UP TIPS FOR CONSUMERS

- The applications filed with ABDRC should contain sufficient information to be reviewed by traders;

- Consumers should submit as soon as possible the information or documents requested by the trader or by the conciliator with a view to settling the applications or conducting the negotiations via ABDRC;

- Increase care is required when filling out the contact date (Personal Numeric Code (CNP), email, phone number), and the email inbox should be checked for any new messages about the start or status of the conciliation procedure;

- Since many consumers sought to have the abusive clauses removed from their loan agreements, we remind them that ABDRC can facilitate renegotiation of the contractual clauses, but conciliation cannot determine whether certain clauses are abusive or not (this can only be done in court);

- Consumers need to provide details about their current situation: medical problems, family problems, reduced income or increased costs. Then, they need to submit documents in support of their account of the facts;

- No legal background, indication of laws or review of the contractual clauses are required to submit an application. The personal situation must be described in summary, with sufficient details, using a plain language;

- An application may only be intended for one single trader. There have consumers that listed more traders in the same application, and an application may not been intended for more recipients. On the contrary, a consumer may file more application for one or more traders;

- Consumers may fill out the application on the website csalb.ro;

- Consumers can receive information about their applications or cases by sending an email to [email protected].

OUTCOME OF THE CONSUMERS-BANKS/NBFIs NEGOTIATIONS

The number of applications received in the first half of 2021 stays relatively flat v the first half of 2020. The inflow of applications continues to be determined by the sanitary crisis. Many consumers became unemployed, or their work was suspended, which could led them into applying for either the statutory moratoria (in the first part of the year), or identification of a solution to rebalance their contractual obligations. Of the total number of applications received by the end of the first half of 2021, 781 concerned different issues in relations with banks, whereas 448 concerned different issues in relations with NBFIs.

The share of applications intended for NBFIs is increasingly higher. While this was 22% of the total in the first half of 2020, in the first half of 2021 it is 36%. Unfortunately, only 3 applications intended for NBFIs were accepted for negotiation in the first half of 2021, compared to 11 in the same period of last year. Also, the number of applications intended for banks decreased in the first semester of this year: from little over 1,000 applications/first half of 2020, down to only 781 applications/first half of 2021 (a decrease of approx. 25%).

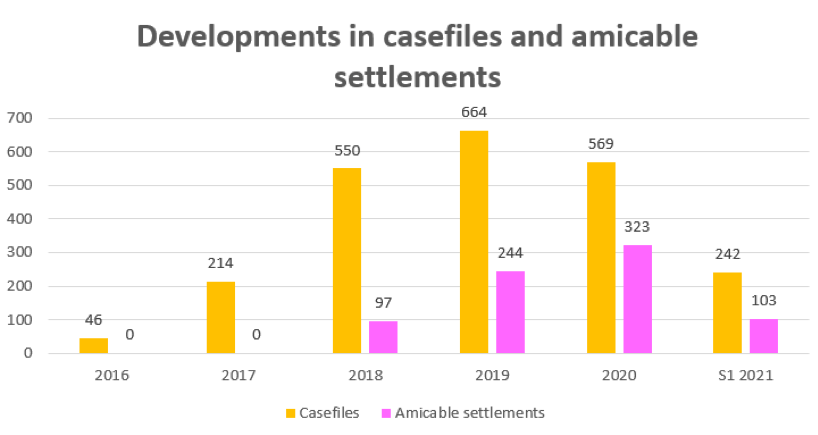

Furthermore, before the end of the first half of 2021, 103 applications were settled amicably by traders after the respective cases having been referred to ABDRC (traders negotiated directly with consumers), broken down as follows: 81 applications settled amicably with banks, and 22 applications settled amicably with NBFIs.

The developments of the past years point to a significant decrease in the number of applications rejected by banks of those received by ABDRC: from 80% in 2016 down to 45% in 2018, and to 28% in 2020. During the first six months of 2021, the share of applications which were unreasonably closed by banks dropped down to 18%, and the recommendation that ABDRC makes to both banks and NBFIs is to strive to keep this percentage below 20% by the end of the year. This is an actionable objective, so much the more that there are already large banks the rejection rate of which ranges has already dropped below 10%, or even below 5%.

About ABDRC: ABDRC is an entity set up under a European Directive, and intermediates, free of charge and in not more than three months, negotiations between consumers and banks or NBFIs, for contracts/agreements in progress. Consumers from any county of the country may file applications with the Alternative Banking Dispute Resolution Centre (ABDRC), filling-in an online form directly on the website www.csalb.ro. When the bank accepts to enter the conciliation/negotiation procedure, a conciliator is appointed. ABDRC works with 19 conciliators, of the best specialists in law and with relevant experience also in the financial and banking field. Everything is settled amicably, and the understanding between the parties has the power of court judgment. More information about the work of the Centre is available by phone at 021 9414 (charged a normal rate).