July 14, Bucharest. During the first half of this year, consumers submitted a record number of requests to negotiate with banks and non-bank financial institutions (NBFIs) through the Alternative Dispute Resolution Center for the Banking Sector (CSALB). The 2,060 requests received represent the highest six-month total in CSALB’s more than 10 years of activity. Moreover, the second quarter of this year was the first quarter in which the number of valid applications exceeded 1,000, reaching 1,092 requests. The 40% increase compared with the first half of 2025 (1,464 requests) reflects the difficult economic environment, both nationally and internationally, as consumers seek solutions to improve their personal financial situation amid the rising cost of living. Regarding the number of conciliation cases, banks entered into approximately 400 negotiations during the first half of the year, while NBFIs did not accept a single negotiation request, despite receiving more than 600 applications.

During the first six months of the year, 332 negotiations ended with an amicable agreement between the parties, representing 91% of all negotiations conducted. The total financial benefits generated through these negotiations approached €1 million, averaging approximately €2,700 per successfully resolved dispute. Additionally, 59 court cases pending before ordinary courts were settled after consumers and banks, following judges’ recommendations or at the initiative of one of the parties, agreed to negotiate through CSALB. The procedure is free of charge for consumers, takes an average of two weeks, and is conducted with the assistance of a conciliator specializing in banking and financial matters. Since 2021, more than 880 lawsuits have been settled amicably through the dialogue framework provided by CSALB.

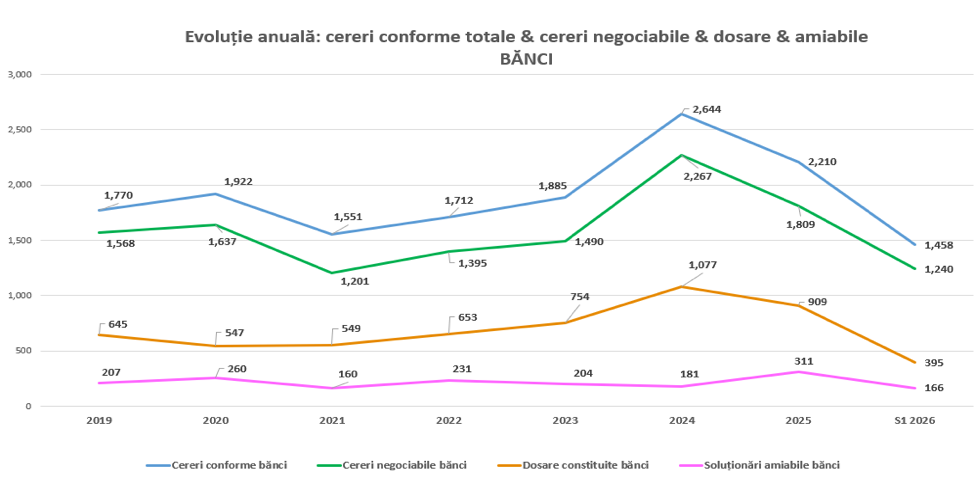

By the end of the first half of 2026, 1,458 requests concerned disputes with banks (compared with 1,095 during the same period in 2025), while 602 requests related to consumers’ relationships with NBFIs (compared with 369 in H1 2025). Requests submitted to NBFIs increased by 63% year-on-year, and their share of total requests rose from 25% in H1 2025 to 29% in H1 2026.

By the end of the first half of 2026, 1,458 requests concerned disputes with banks (compared with 1,095 during the same period in 2025), while 602 requests related to consumers’ relationships with NBFIs (compared with 369 in H1 2025). Requests submitted to NBFIs increased by 63% year-on-year, and their share of total requests rose from 25% in H1 2025 to 29% in H1 2026.

By the end of H1 2026, 202 requests had been resolved directly between financial institutions and consumers following CSALB’s intervention: 166 requests settled directly by banks; 36 requests settled amicably by NBFIs.

During the same period in 2025, banks resolved 91 requests, while NBFIs resolved 32. Compared with last year, the number of requests settled directly by banks has nearly doubled.Maintaining this practice of direct amicable settlement after CSALB notification provides consumers with an additional dispute resolution channel, particularly for simpler cases that do not necessarily require the expertise of CSALB conciliators. Banks have made greater use of this approach than NBFIs.

The Most Common Consumer Requests. Approximately 90% of all requests concern loan agreements and include:

- refunds of fees and interest;

- reductions in outstanding loan balances;

- lower monthly installments;

- cancellation of overdue payments;

- loan rescheduling, refinancing, renegotiation, or contract rebalancing, including cases involving hardship or unforeseen circumstances.

Consumers also frequently request:

- general solutions for reducing borrowing costs;

- switching from the ROBOR reference rate to IRCC;

- foreign currency loan conversion;

- interest recalculation;

- payment restructuring agreements;

- removal of certain contractual clauses.

Other requests concern:

- deletion of negative records from the Credit Bureau;

- reinstatement of repayment schedules for borrowers subject to enforcement proceedings;

- switching to fixed interest rates;

- withdrawal of court actions;

- resolution of disputes arising from banking fraud.

Higher Quality Requests

In the first half of 2026, 84% of all requests were eligible for negotiation, compared with 78% during the same period in 2025 and 65% in 2024.

This improvement is largely due to the decline in requests seeking deletion of Credit Bureau records—cases that cannot be handled through CSALB negotiations but must instead be resolved directly between the parties or dismissed. Their number fell from:

- 669 in H1 2024,

- 321 in H1 2025,

- 340 in H1 2026 (despite the significant increase in total requests).

The number of negotiation cases reached 395 in H1 2026, compared with 415 in H1 2025.

Of the 1,240 negotiable requests submitted to banks, 395 were converted into formal negotiation cases. By contrast, NBFIs did not agree to open negotiations for any of the 480 negotiable requests they received.