A WARNING FROM ABDRC: NBFIs DON’T GET ALONG WITH CONSUMERS EASILY

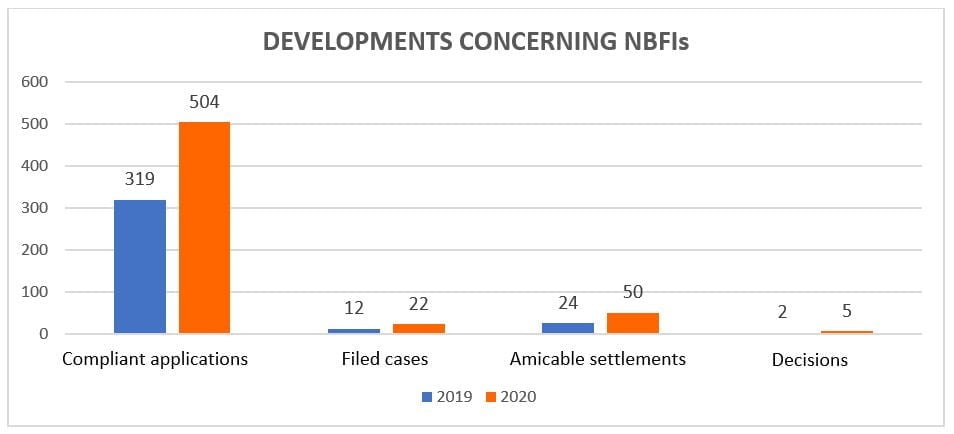

Conciliation between Non-Banking Financial Institutions (NBFIs) and their clients is still rather shy in terms of results, even after five years of operation of the Alternative Banking Dispute Resolution Centre (ABDRC). While there are 60% more applications filed with NBFIs this year compared to last year, the Non-Banking Financial Institutions only agreed to negotiate on 22 such consumer applications. Of these, in only five cases the negotiations concluded with an agreement between the parties, which is 55 times less than in the case of banks. Unfortunately, this year only two NBFIs accepted to engage in negotiations with consumers via ABDRC.

Only two NBFIs engaged in conciliations with consumers

The approximately 500 applications concerned more than 25 NBFIs and Mutual Aid Funds (MAFs). The bulk of the applications were filed with: Cetelem, Eassy Asset Management, Unicredit Consumer Financing, Provident, BT Direct IFN and CreditEurope Ipotecar IFN.

Unfortunately, this year only two NBFIs accepted to engage in negotiations with consumers via ABDRC: Credit Europe Ipotecar IFN and Axi Finance IFN. So far, negotiations have concluded with the parties accepting the solutions proposed by the Centre’s conciliators in only five cases.

“We are worried about the statistics concerning NBFI conciliation, even if, in the first ten months of this year, we’ve seen twice more cases formed or applications addressed directly by the two parties than last year. This number, even doubled, is still insignificant and, unfortunately, only one NBFI proved they grasped the benefits of conciliation and entered into a number of negotiations with their consumers, some of which were successful. Other NBFIs argued, in support of their lack of engagement and reaction to consumers’ applications, that there are several legislative initiatives that, once effective, would reduce their business significantly, or could have adverse effects that can go as far as forcing them to close their business. Some of these initiatives were submitted to the Constitutional Court for review and are still in different law-making stages in the Parliament.

Even under these circumstances, I cannot find a justification for the lack of interest shown by certain NBFIs, which received dozens of applications from consumers, but have not acted upon them in any way. The unreasonable closure rate of these applications exceeds 50 percent. This figure is too high for a market that competes with the banking market, and that needs their consumers’ satisfaction and trust. 2021 will be a difficult year, including for NBFIs, because we expect consumers to face even more difficulties in repaying their loans, while seizures and other enforcement measures should be replaced by negotiations in which consumers work together with their non-banking creditors, and not take opposite sides in courts. Unless both sides conduct a real dialogue and are willing to compromise, we won’t be able to overcome the difficult times ahead of us on the financial-banking and non-banking market next year”, says Alexandru Păunescu, President of ABDRC Steering Board.

Examples of negotiations between consumers and NBFIs

Successful negotiations: In one case, the consumer asked for the repayment schedule to be restored and renegotiate the loan agreement in CHF. The conciliator proposed the consumer to pay the amount of CHF 3,100, accounting for 25% of the remaining interest, and to the NBFI to write off the balance of 75% of the remaining interest, meaning CHF 9,250. Additionally, the interest to day was reduced by 1 pp for a 36-month period.

In another case, regarding a loan in CHF, the consumer asked for the management fee to be eliminated. The conciliator proposed the elimination of this fee for a 30-month period, a solution that was accepted by both parties.

Failed negotiations: In another case, the conciliator proposed that the monthly management fee should be reduced to 0.10%, and calculation of the interest according to Libor 6M+2.5%. While the consumer accepted the solution, the trader rejected it.

In case of a consumer claim for repayment of the management fee and interest adjustment, the conciliator proposed a number of measures: flat interest rate; repayment of the financing fee of CHF 2,500; repayment of the management fee paid to date and its removal from then on. While the consumer accepted the conciliator’s proposal, the NBFI representatives replied that they were unable to make the concessions proposed, arguing that the loan-related fees were lawful and there was no justification for having them removed. But in most of the cases, the claims of consumers and what the trader was willing to offer were so divergent that conciliators could not propose a solution that would address them to the satisfaction of both parties.

Closure of some cases occurred for objective reasons, and the parties didn’t get to negotiate: for the top 2 NBFIs in terms of the number of applications received by ABDRC, deregistration from the Credit Office accounted for approximately 50% of the total, with other 9 applications concerning debts assigned to other companies. In both instances, the powers of ABDRC are rather limited because these claims fall under the scope of special pieces of legislation, or concern companies outside the National Bank of Romania’s supervision or regulation jurisdiction.

What do the representatives of the NBFI, which accepted the highest number of consumer negotiation applications, say:

“We are always open to discuss and find solutions for our contractual partners, when they have difficulties in discharging of their payment liabilities. The key benefit of a successful procedure via ABDRC is that the parties identify a way of moving forward with the contract together, with confidence that the solution obtained is reasonable for them.

The classical court proceedings are longer and more expensive, with strict settlement limitations which do not help take the middle way. Then, the solution proposed by the ABDRC conciliator is not binding for the parties, as a court judgment would be, because this should be accepted by both parties further to conciliation. Thus, when the NBFI and the consumer agree on the proposed solution, there is certainty that a genuine settlement was reached, that meets the needs and wishes or both parties and helps them continuing with their contractual relations trusting one another”, says Daniel Ilie, General Manager of Credit Europe Ipotecar IFN.

The higher number of direct settlements between NBFIs and consumers (with the consumer having first approached ABDRC) is an indication that some traders prefer this alternative in order not to pay the cost of conciliation (lei 993 for each case). While last year saw only 25 amicable settlements in its first 10 months, 50 such settlements have already been reported during the same period of this year.

About ABDRC: ABDRC is an entity set up under a European Directive, and intermediates, free of charge and in not more than three months, negotiations between consumers and banks or NBFIs, for contracts/agreements in progress. Consumers from any county of the country may file applications with the Alternative Banking Dispute Resolution Centre (ABDRC) filling-in an online form directly on the website www.csalb.ro. When the bank accepts to enter the conciliation/negotiation procedure, a conciliator is appointed. ABDRC works with 19 conciliators, of the best specialists in law and with relevant experience also in the financial and banking field. Everything is settled amicably, and the understanding between the parties has the power of court judgment. More information about the work of the Centre is available by phone at 021 9414 (charged a normal rate).