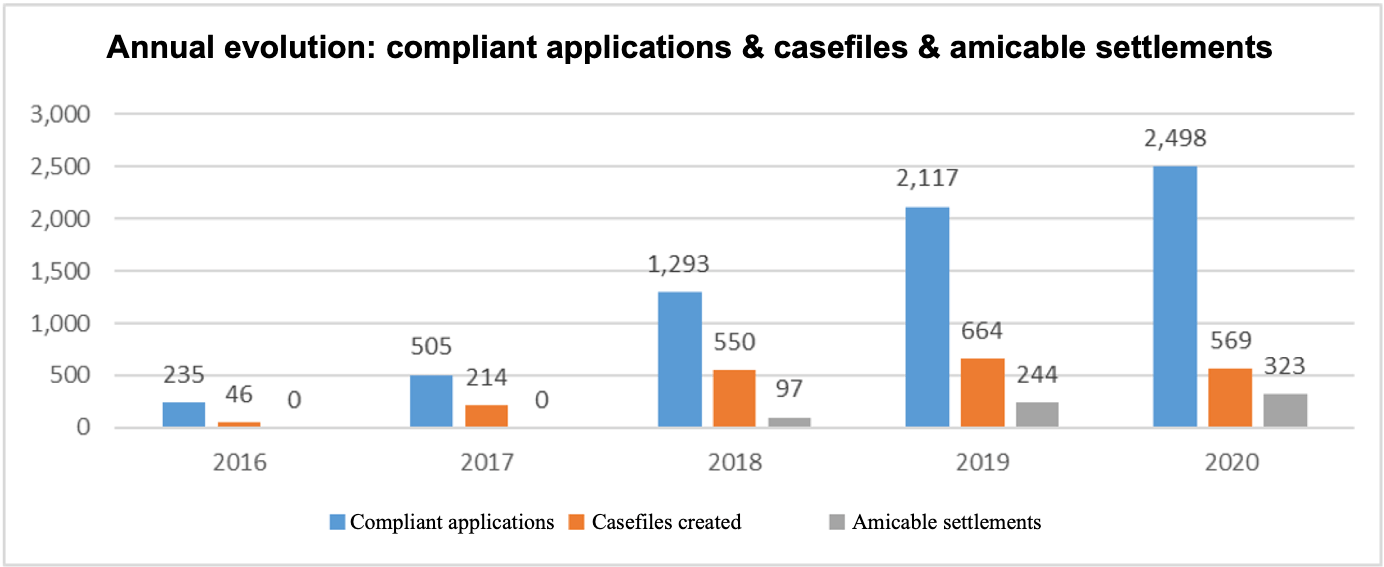

In 2020, ABDRC celebrated their fifth anniversary. During all this time, ABDRC brought along a new paradigm for both banks, and consumers. Conciliation via ABDRC should become the alternative of choice for a consumer when they need to address a problem with the traders in the financial and banking system, to the detriment of the actions brought before courts or other litigation-based methods. The active involvement of both parties in contract negotiation, facilitated by an independent expert, the conciliator, has started to shape a shift in the past and still current perception of the contracts and commercial services, or of the banking services.

I. About ABDRC Establishment

- The Alternative Banking Dispute Resolution Centre (ABDRC) is an independent non-governmental apolitical, not-for-profit legal entity of public interest established under the Government Ordinance no. 38/2015 on alternative resolution of disputes between consumers and traders, which transposes at domestic level Directive No 2013/11/EU on alternative dispute resolution (ADR) for consumer disputes, as well as Regulation (EU) No 524/2013 of the European Parliament and of the Council of 21 May 2013 on online dispute resolution (ODR) for consumer disputes.

As between the consumer and the bank, alternative dispute resolution (ADR) sets out the best possible framework for the dialogue between the parties, and fosters running of reliable analyses on the aspects reported by consumers, in view of identifying and addressing, as applicable, the deficiencies and the potential incorrect practices in the work of professionals.

Additionally, further to transposition by Romania of the Payment Services Directive/PSD2, the following laws were passed:

- Law no. 209/2019 on payment services, and amending certain items of legislation

and

- Law no. 210/2019 on the issuing of electronic money,

the subject-matter jurisdiction of ABDRC was extended so as to cover a new category of subjects, namely “users that are legal entities“, considering their capacity of users of payments services, and/or the violation by the issuers of electronic money of the legal provisions laid down in the regulations above.

- ABDRC’s work is render at two levels:

- administrative – organization and functioning of ABDRC as legal entity;

- operational – organization and performance of the alternative dispute resolution activity.

The aim of this keeping these two lines of work separated is to reflect the independence of the Conciliators’ work from the administrative matters of ABDRC.

II. Administrative activity of ABDRC

1. Activity of the Steering Board

The ultimate duty of the Board, the work of which is rendered under the Regulation for ABDRC’s Organization and Steering Board’s Functioning, is to steer and provide oversight of the administrative activity of the Centre. Thus, the members of the Steering Board have powers and duties in connection with approval and amendment of the resolution procedures, approval of conciliators, approval of the income and expenditure budget, etc.

The Board members are not involved in any operational activity of the Centre (the review and resolution of the disputes being reserved exclusively to conciliators), and their task is to see that ABDRC has available sufficient resources to carry out its activity in an efficient and independent manner.

Highlights of the Steering Board’s activity in 2020:

- drawing up and approval of the two ADR Procedure Regulations for legal entities further to extension of the ABDRC’s scope of work to cover also for legal entities that access the services regulated by Law no. 209/2019 and Law no. 210/2019;

- ordering adaptation of all activities (conciliation, meetings of the Steering Board, communication, employees’ presence in the office, meetings with traders/collaborators, etc.) to the current COVID-19 pandemic context, in appropriate security conditions;

- continuation of the administrative litigation proceedings registered with Bucharest Court of Appeal under case number: 6047/2/2018, concerning the challenge of ABDRC against the Decision no. 2377/DA/31.05.2018 issued by the Ministry of Economy on entering ABDRC in the list of ADR entities in Romania – the proceedings are pending before this court;

- resuming/following up on the efforts to engage the NBFIs in the activity of the Centre;

- approval of the financial statements executed as at 31 December 2019;

- performance/development of the communication activity via different channels adapted to the current COVID-19 pandemic context, in appropriate security conditions;

- the end of the 5-year offices of the members who sat in the first Steering Board;

- arranging for the institutions represented in the Steering Board to issue the new 5-year mandates for their new representatives therein;

- election of the independent member of the Steering Board for a 5-year term of office;

- election of the President of the Steering Board of a 1-year term of office;

- reviewing the draft 2021 budget and approval of ABDRC’s 2021 budget (2021 IEB).

2. Communication, promotion, information and financial education

Communication takes place across the following levels (according to ABDRC’s communication strategy):

- communication with banks and NBFIs (traders);

- communication with consumers;

- communication with stakeholders;

- holding of work meetings with conciliators, whenever these are necessary, as part of the process of updating/reviewing the Regulation of the Procedural Secretariat and the ADR procedures, as the amicable dispute resolution work advances;

2.1. ABDRC’s Communication and Promotion Activity

Communication with, and information of consumers and traders about ABDRC take place via the following channels:

- communication via the traditional media channels (TV, Radio, Written Press, Online, Blogging);

- communication via own channels: Website, Facebook, LinkedIn, YouTube, Instagram;

- organization of/participation in conferences, seminars, debates (also online), etc.;

- communication via commercial banks (online and offline: fliers, posters, stickers, candy crayons sent to the banking agencies, video productions);

- communication via the National Authority for Consumer Protection (at central level and through the County Commissariats);

- communication via consumer associations.